Looking into Malaysia’s Push for Ethical Lending

The COVID-19 pandemic reshaped how Malaysians accessed credit. With incomes disrupted and financial uncertainty looming, more consumers and businesses turned to alternative lending options. Services like Buy Now, Pay Later (BNPL) made purchases easier for consumers and small businesses, while other enterprises made use of leasing and factoring to maintain cashflow.

All this initially went well, but as time went on, cracks started to show.

Without clear regulations, many consumers unknowingly accumulated high debt across multiple BNPL providers, businesses struggled with opaque leasing and factoring agreements, and unlicensed debt collection agencies would often resort to harassment, intimidation, and unethical recovery tactics.

The Consumer Credit Act (CCA) was introduced to fix this broken system—creating a fairer, more transparent, and well-regulated consumer credit ecosystem.

What is the Consumer Credit Act (CCA) Malaysia?

Announced in 2022, the Consumer Credit Act (CCA) is Malaysia’s response to the “wild west” of consumer credit, setting clear rules and protections to ensure fair and responsible lending and debt recovery practices.

The CCA’s Scope Covers Six Key Financial Services:1

- Buy Now, Pay Later (BNPL) – Protecting consumers from debt traps caused by multiple BNPL accounts.

- Leasing – Ensuring transparency in lease agreements and affordability assessments.

- Factoring – Regulating financial services that help businesses manage cash flow through invoice financing.

- Debt Collection Agencies – Setting strict guidelines on ethical and legal debt recovery.

- Impaired Loan Buyers – Regulating firms that purchase non-performing loans (NPLs) and ensuring fair practices.

- Debt Counselling & Management Agencies – Standardizing financial counselling and restructuring services.

The CCA’s main goals are three-fold:2

- Regulate credit providers and credit service providers;

- Encourage proper conduct and responsible lending in the credit industry;

- Promote a fair, efficient, and transparent credit industry.

How the Consumer Credit Acton Pushes for Greater Accountability and Transparency

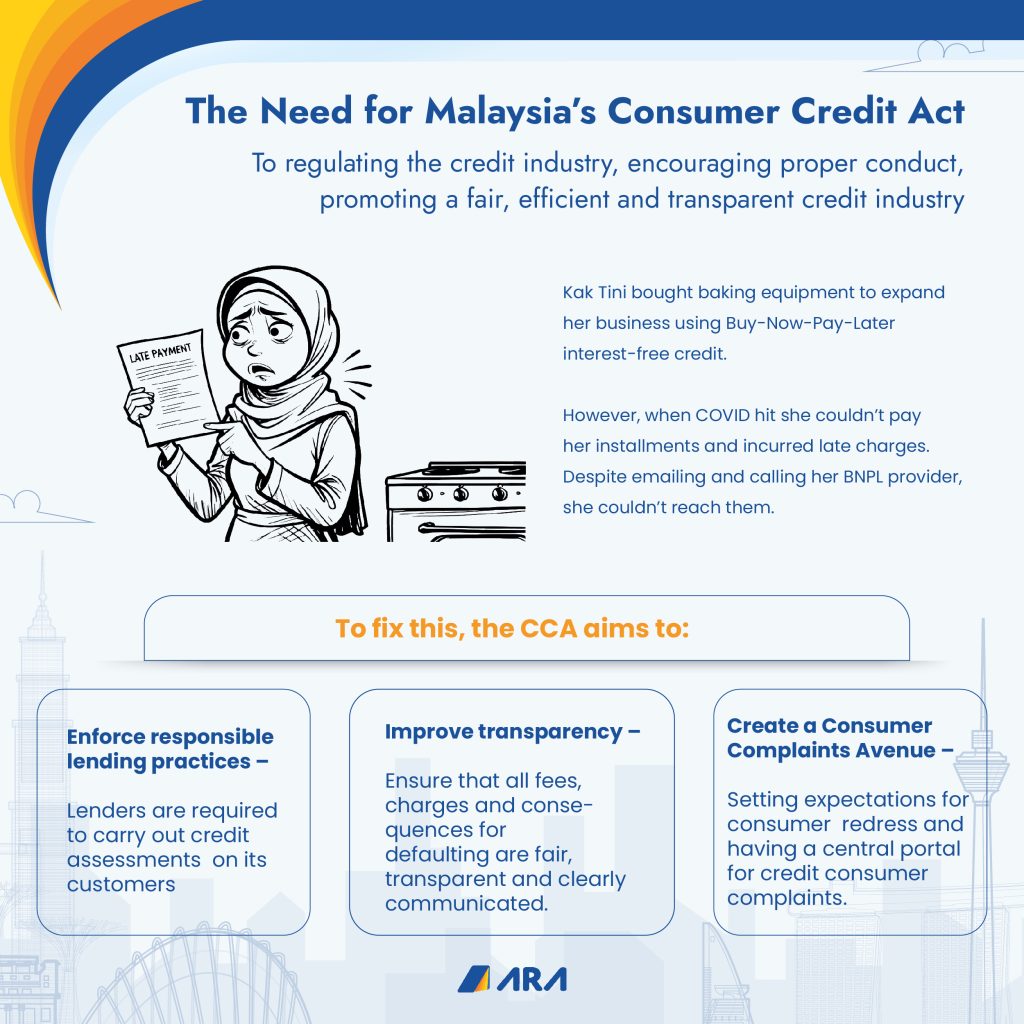

Take Kak Tini, a home-based baker who used BNPL to purchase baking tools to expand her business. Drawn in by the promise of interest-free credit with seemingly no strings attached, she used the credit to buy top of the line baking tools for her business.

But then COVID occurred, blocking her cashflow as she was unable to run her business. As she missed installment payments, she was shocked that she was incurring late payment fees.

In her haste for instant credit and her lack of digital-savvy, she agreed to the terms and conditions set by her BNPL provider – not realising what would happen if she missed payments. Worse still, her calls and emails to the BNPL provider were not attended to and she is unsure if there are any avenues for redress.3

This is where the Consumer Credit Act steps in:

- Credit providers, including BNPL players must now assess repayment ability before approving credit—no more unregulated instant approvals.

- Transparent loan terms—no hidden fees or misleading zero-interest claims.

- A centralized complaints system—so consumers like Kak Tini can challenge unfair treatment.

Credit providers such as BNPL services aren’t going away—but under the CCA, it will operate with clearer rules and greater accountability.

Ending Harassment & Illegal Debt Collection Practices

Debt collection in Malaysia has long been a high-pressure, low-trust industry.

Harassment posters. Threatening phone calls. Fake debt collectors showing up at people’s homes. This has been the reality for many borrowers. The lack of regulations allowed unethical debt collection agencies to use intimidation tactics—until now.

A New Straits Times report at the beginning of 2025 highlighted a retiree being harassed by self-proclaimed debt collectors, even though he didn’t owe them anything. (Read more here).

Under the Consumer Credit Act, debt collection will be strictly regulated:

- Only licensed debt collectors can operate—no more fake “agents.”

- Credit and credit service operators need to be authorised with the Consumer Credit Oversight Board, the relevant regulatory and supervisory authority.

- Pushy, misleading, or aggressive tactics will be punishable by law.

- This includes a fine or imprisonment (Draft CCA Consultation Phase 2 – Section 9.4)4

- A White List of authorized lenders and agencies will help consumers verify legitimate providers.

- The CCOB will run a one-stop portal listing authorized credit providers and services, allowing the public to verify their legitimacy. (Draft CCA Consultation Phase 2 – Section 1.14)5

- Debt collectors must carry official authorization cards before approaching consumers. (Draft CCA Consultation Phase 2 – Section 15.4)6

This means borrowers can finally differentiate between legitimate recovery efforts and intimidation tactics.

What Malaysia’s Consumer Credit Act This Means for BNPL, Leasing, Factoring & Lenders

If you’re a financial institution, BNPL provider, leasing company, or debt collection agency, the Consumer Credit Act means one thing:

🔹 Compliance is no longer optional.

You’ll need to:

- Conduct affordability assessments before offering credit—for both consumers and businesses.

- Follow standardized debt collection protocols—no aggressive tactics, misleading information, or unauthorized recovery methods.

- Ensure clear, transparent loan terms to prevent customer disputes.

The big opportunity? Businesses that adopt ethical, compliant debt collection and lending strategies now will gain a major competitive advantage.

How ARA Pay is Leading the Way with AI-Powered Ethical Collections

At ARA Pay, we’ve always believed in ethical, AI-powered debt recovery—long before the Consumer Credit Act came into play.

Here’s how we’re already aligned with the new regulations:

- WhatsApp-based AI collections – No spam calls, just friendly, automated reminders.

- Flexible repayment options – AI engages debtors to find personalized solutions like financial planning or restructuring.

- Compliance-first approach – We ensure businesses stay within CCA guidelines while improving recovery rates.

The future of debt collection isn’t about pressure—it’s about smarter, solution-focused engagement.

Is Your Business Ready for the CCA?

The Consumer Credit Act isn’t just about protecting consumers—it’s about reshaping the financial industry for the better.

For businesses, compliance isn’t just about avoiding penalties—it’s about building trust.

If you’re a BNPL provider, lender, leasing company, or debt collection agency, now is the time to adopt AI-powered, ethical debt collection strategies.

How do you think the Consumer Credit Act will impact debt collection in Malaysia? Let’s discuss.

References:

- CCOB Task Force

- Consumer Credit Act – Public Consultation Paper Part 1 Page 6

- Consumer Credit Act – Public Consultation Paper Part 1 Page 18

- Consumer Credit Act – Public Consultation Paper Part 2 Section 9.4

- Consumer Credit Act – Public Consultation Paper Part 2 Section 1.14

- Consumer Credit Act – Public Consultation Paper Part 2 Section 15.4

Leave a Reply